WASHINGTON — A Union Pacific-Norfolk Southern merger would reduce shipping options for farmers and make them more vulnerable to price increases, economists for the American Farm Bureau said in an analysis released today (Wednesday, March 11).

The long-term effect of the merger could be increased consumer prices for food as expenses rise throughout the food supply chain, the Farm Bureau cautions, and says it opposes the merger as a result.

The Market Intel report says the merger “would leave farmers more dependent on fewer railroads at a time when they already have almost no ability to walk away from higher costs or poor service. The merger does not create new competition for agriculture. It removes what little leverage remains by eliminating key routing and interchange options that currently help keep rates and service in check.”

A combined UP-NS merger would account for approximately 44% of originated carloads in major commodity groups, the report says, citing Surface Transportation Board and U.S. Department of Agriculture data. “In practical terms,” it says, “this would leave large portions of the country dependent on a single railroad for end-to-end service, eliminating key interchange points, such as Chicago, St. Louis, or New Orleans, where shippers could previously bargain between UP and NS.” This matters in an agricultural context, it continues, because of the already limited local competition, as illustrated by the fact approximately 95% of grain elevators are served by only one railroad.

“In these settings,” the report says, “competitive discipline does not come from the ability to switch carriers, but from regulatory oversight that substitutes imperfectly for market forces.” It also notes that bulk commodities, especially grain, have limited ability to move to another mode of transport: “Trucking long distances significantly increases per-unit costs, while barge access is geographically limited.” As a result, “Grain shippers served by fewer railroads or located farther from barge terminals consistently pay higher rates per ton-mile than similarly situated shippers with more transportation options.”

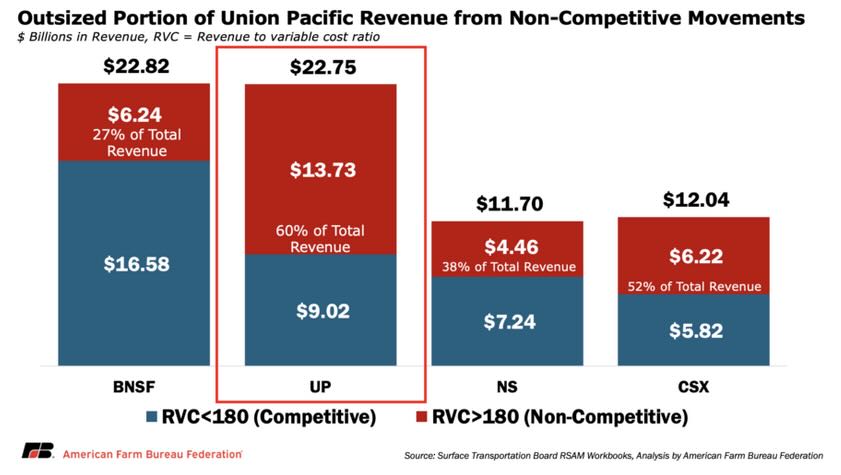

The report says Union Pacific already gains about 60% of its total revenue from markets with many captive shippers and few transportation options — a larger percentage than the other three U.S.-based Class I railroads. UP has the industry’s largest carload network.

If the merger’s promised growth and gains in efficiency do not materialize, the report says, “the financial obligations of an $85 billion acquisition still must be recovered. In a system where agriculture is already carrying a growing share of rail cost recovery, those pressures will not fall evenly. They will fall where alternatives are few and demand cannot adjust.

“For farmers and rural communities, this merger is not about bigger trains or faster routes. It is about who has choices and who does not, and whether the risks of consolidation are borne by shareholders or by the people who depend on rail to get their crops to market.”

UP and NS say their merger will make American farmers, and industry in general, more competitive in global markets through factors such as decreased transit times [see “CEOs say … merger will spur traffic growth,” Trains.com, July 29, 2025]. And UP CEO Jim Vena told a shippers’ conference in January that the efficiencies of the merger would give the combined railroad “an opportunity to not price as much” [see “Union Pacific CEO tells customers …,” Jan. 15, 2026].

— To report news or errors, contact trainsnewswire@firecrown.com.

Share this article