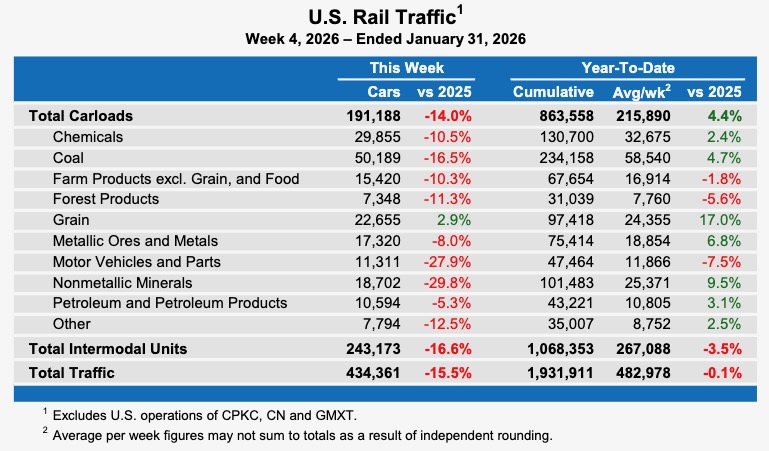

I recently sifted through each of the publicly traded Class I railroads’ third-quarter earnings webcasts to get a consensus on revenue and volume expectations headed into the New Year [see “What Wall Street analysts are asking …,” Trains News Wire, Dec. 6, 2024]. A consistent theme is railroads are pricing above inflation. This means that freight rates are above current inflation rates. In October, that rate was 2.6%.

Protecting the operating margin and hedging against inflation through price is understandable. Railroads are also keeping the house clean and finding productivity across crafts and processes. This, combined with improved service, bolstered headcounts, and resiliency are all commendable efforts. For the first time since I’ve been in the business, I feel like railroads are ready for new volume and can ramp up easier than before.

But new volume is key. Freight and especially truck markets are soft. There’s nearshoring and manufacturing optimism associated with the new administration, but it won’t happen quickly. Will proposed new tariffs cause inflation to increase? Can railroads outrun inflation to protect the operating ratio if inflation returns to 4-5%? Can the U.S. manufacturing sector maintain its output at sustained levels of higher inflation? And will running ahead of inflation entice new rail business, given all of the truck capacity?

My biggest concern is railroads will price above a higher inflation rate to protect the margin in a volume-soft environment. I’m concerned higher-for-longer inflation could lead to volume erosion if truck capacity remains robust. I’m certain railroads are asking these same questions.

These are all questions that I’m seeking the answers to as we head into 2025. I want railroads to get it right. I want to see railroads capture meaningful amounts of new volume. Volume should be the reward for the hard work railroads have achieved in cleaning up their networks and hiring for growth.

With a lot of large union agreements now ratified, railroads can better predict labor costs in the near term. Fuel is also trending downward. The four big Class I railroads have all saved more than $100 million in fuel this year compared to last, and Union Pacific’s fuel cost is down $239 million year over year. This correlates to fewer fuel surcharge revenues, but overall, this is a major savings.

And while railroads have touted that price dollars are outrunning inflation dollars, I do want to recognize that railroads’ average revenues per unit (RPU) have increased modestly year over year. Outside of declining index-based coal pricing and softer intermodal rates, the big four Class I railroads have priced conservatively in 2024.

Union Pacific’s industrial rates are up 4%; CSX Transportation merchandise rates up 2%; Norfolk Southern merchandise up 1%; and BNSF Railway’s industrial rates are flat. U.S. inflation has decreased more than 1% since last year. Railroad rates do seem to be moving in tandem with inflation, which is encouraging.

But, honestly, all of this talk about inflation is getting old. As far as railroads are concerned, I want the conversation to shift from inflation to the benefits of a reliable rail supply chain. Railroads’ operating performance is the best it’s been in a while — and while you can price for reliable service to some extent, a stronger economy in a deflationary environment could win the railroads great volume success.

And perhaps railroads can still win in a high inflationary environment. I’m definitely no economist. But the idea of pricing above inflation, especially if it increases again, with so much truck capacity doesn’t feel like a winning solution for carload growth.

Share this article