Intermodal has long been the rail industry’s growth engine. But it hasn’t been firing on all cylinders in recent years. Yes, 2018 was a record-setting year for volume, and 2021 was intermodal’s second-best year ever. That’s all well and good — except that intermodal hasn’t been keeping pace with economic growth and has lost market share to the highway.

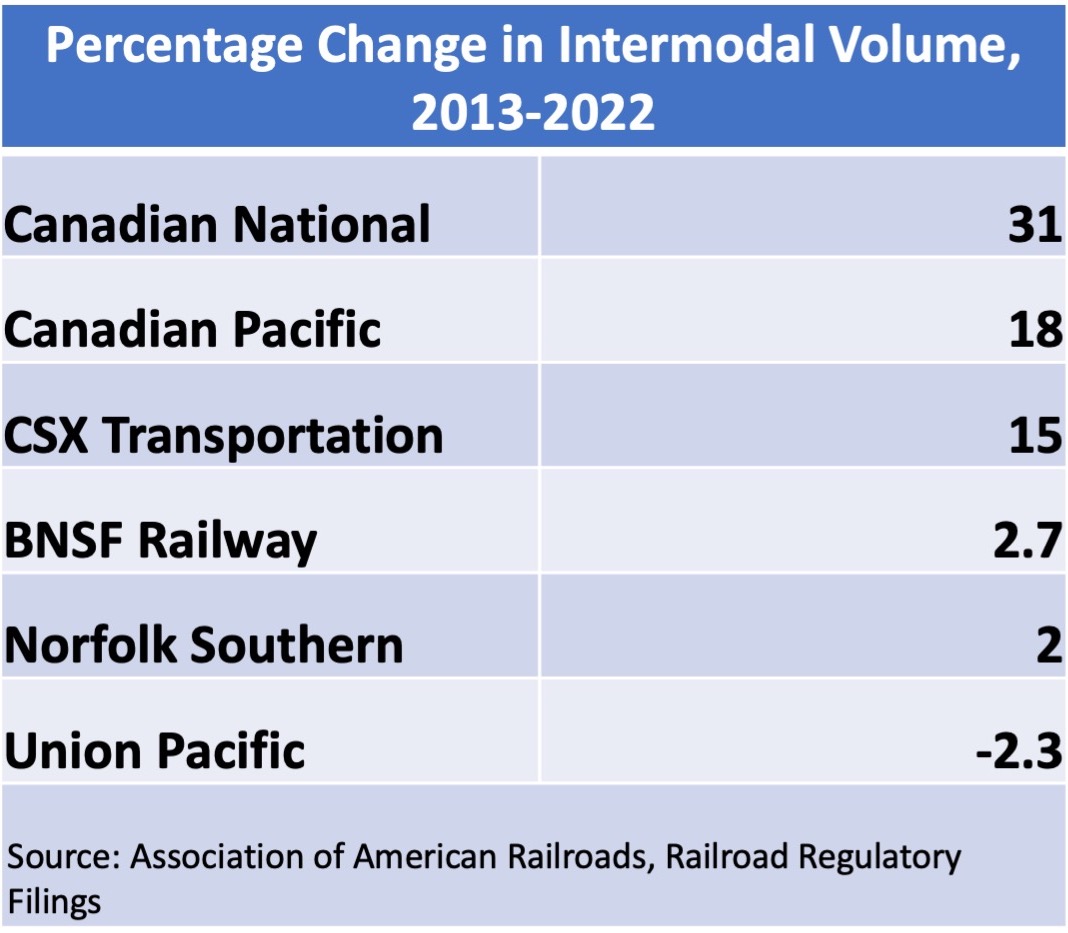

As intermodal analyst Larry Gross points out, since 2015 the economy has expanded at a compound annual growth rate of 2%, import container volume has grown at a 5.3% pace, and long-haul truckloads have increased 3.5% annually. Total intermodal volume has lagged. It’s grown at just an average of 0.2% since 2015, with domestic volume growing at an 0.9% clip and international volume shrinking by an average of 0.7% annually.

“Seven years of underperformance cannot be explained away by special circumstances and one-off issues,” Gross says. “The intermodal offering in its current form is not resonating with its target markets. Is it realistic to expect that intermodal will suddenly regain traction if nothing changes in what it is offering to its customer base?”

That’s an important question for the industry, especially when you consider that the thermal coal used to generate electricity is going away and most carload commodities are stagnant or declining. If railroads are to see meaningful growth, intermodal has to lead the way.

You can point to a bunch of factors that are behind intermodal’s anemic performance:

- The ongoing shift of imports to the East Coast, which makes containers less likely to ride the rails compared to boxes that arrive at West Coast ports.

- Norfolk Southern’s 2015 decision to pull the plug on its Triple Crown RoadRailer network, leaving it with just the Detroit-Kansas City lane. The rest of Triple Crown’s volume migrated back to the highway.

- The pruning of steel-wheel interchange in Chicago as railroads implemented Precision Scheduled Railroading and simplified their intermodal networks in 2017-18. Service was dropped altogehter between many origin-destination pairs.

- Rapid growth in trucking during the pandemic, when kinks in the supply chain made cargo owners prioritize speed.

But by far the biggest reason why intermodal growth has slowed is unreliable service. The one-two punch of crew shortages and intermodal terminal congestion has clobbered rail service over the past couple of years. So loads have hit the roads.

Most of that traffic will be perfectly happy to return to intermodal once service rebounds to normal levels, says Oliver Wyman consultant Adriene Bailey, who has experience as an intermodal customer and as a railroader at CSX Transportation and Southern Pacific.

But railroads will have to get much more reliable if they want to rev up intermodal growth. Even when railroads are operating well, intermodal trains may arrive 5 to 10 hours ahead of schedule or up to a day late. “With that wide range of variability, how are you ever going to get a reliable service product?” Bailey asks. “In order for railroads to take share, they have to get service right.”

Beyond becoming more reliable there’s no one answer to reigniting intermodal growth.

Railroads could be more flexible on pricing on a lane-by-lane basis, which Bailey says would allow them to attract new domestic traffic. Railroads also need to figure out how to be more effective competitors in short-haul intermodal lanes as more imports arrive at East Coast ports that are closer to inland consumers, she says.

Gross says railroads need to do three things to break out of the intermodal doldrums.

First, they need to develop more robust networks that serve secondary markets. “They need to get away from the skeletal network concept where volume is gathered by long drays and then put on massive trains,” he says. “Railroads keep trying to impose a simple network on a market that’s inherently complex.”

Second, they need to introduce new services aimed at medium lengths of haul. A prime example would be connecting cities that are within 500 miles of the Mississippi River, the de facto dividing line between the eastern and western railroads. Except for Norfolk Southern-Kansas City Southern interline service linking Dallas and Atlanta via the Meridian Speedway, railroads don’t really serve so-called watershed traffic.

Third, they need to figure out how to become a viable competitor to trucks. “The industry needs to stop thinking there’s some exterior force that’s going to push traffic back to the railroad,” Gross says, citing things like a shortage of truck drivers, high fuel prices, and shippers’ desire to reduce emissions by shifting freight from road to rail.

Instead, he says railroads need to offer the right combination of service, reliability, and rates that will attract traffic from the highway. In other words, railroads need to make shippers want to use intermodal.

There’s a massive incentive for retailers to move consumer goods by rail due to their aggressive goals to reduce greenhouse gas emissions. Intermodal is like an easy button because its carbon footprint can be up to 75% lower than truck, according to railroads’ online carbon estimator tools.

Environmental concerns will be an effective tiebreaker for shippers considering intermodal, Gross says. “But if the choice is substandard service and paying more, it’s a pipe dream,” he says of growth tied to reducing emissions.

The combination of an intermodal volume lull and a return to full train-crew staffing is expected to allow the big four U.S. railroads to get service back to normal levels by midyear. The trick will be to maintain service – and then improve it – so that intermodal customers gain the confidence they need to put more volume on rails.

You can reach Bill Stephens at bybillstephens@gmail.com and follow him on LinkedIn and Twitter @bybillstephens

Share this article